.avif)

Mortgage News

FHA Mortgage Credit Score Guidelines: What First Time Buyers in Washington Should Know

For many first time homebuyers, one of the biggest concerns is whether their credit score is high enough to qualify for a mortgage. Questions like "Do I have the right score?" or "What is the minimum score required?" are common among borrowers beginning their homeownership journey.

The good news is that FHA loans are designed to expand access to homeownership, making them one of the most popular financing options for buyers with limited credit history or less than perfect credit.

Understanding FHA mortgage credit score requirements, how lenders evaluate your financial profile, and what factors influence approval can help Washington homebuyers prepare for a successful mortgage application.

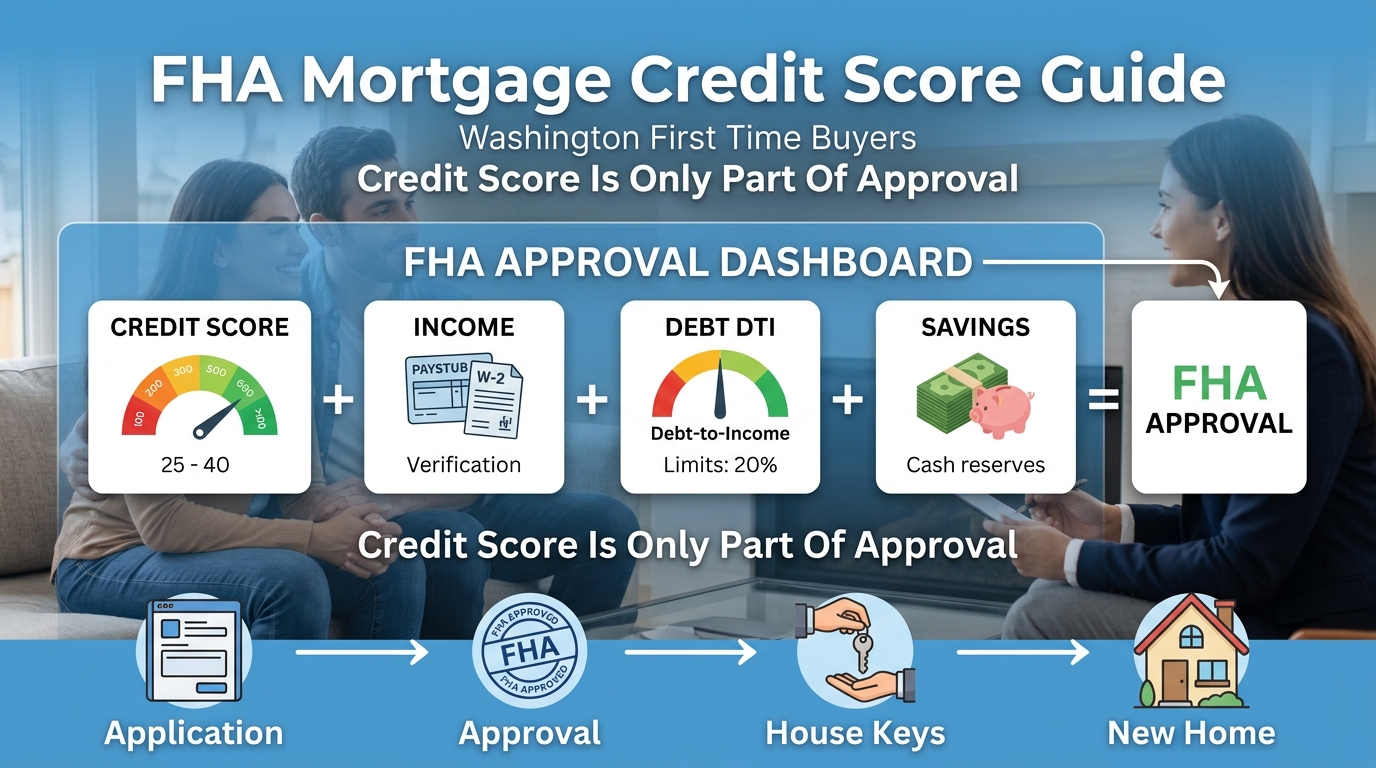

While your credit score is important, it is only one part of the overall underwriting process.

Why Mortgage Credit Scores Matter

Every mortgage application begins with evaluating risk.

One of the first indicators lenders review is your mortgage credit score.

Your credit score helps lenders understand how you have managed financial obligations over time.

It reflects factors such as:

- Payment history

- Outstanding debt

- Credit utilization

- Length of credit history

- Credit mix

- Recent credit inquiries

A stronger credit profile generally provides borrowers with access to more financing options and competitive mortgage terms.

Key Takeaway

A mortgage credit score helps lenders evaluate financial responsibility and plays an important role in mortgage approval decisions.

What Is the FHA Mortgage Credit Score Requirement?

Many buyers ask:

What FHA mortgage credit score is required?

The FHA establishes minimum eligibility standards, but individual lenders may apply additional requirements known as lender overlays.

While qualifying scores can vary depending on the lender and overall borrower profile, approval is based on much more than credit score alone.

Lenders also evaluate:

- Income

- Employment history

- Debt to income ratio

- Down payment

- Assets

- Overall financial stability

For many Washington borrowers, FHA financing provides greater flexibility than some conventional mortgage programs.

Key Takeaway

The FHA mortgage credit score requirement is only one part of the qualification process. Lenders also evaluate your complete financial profile before approving a loan.

Mortgage Credit Score Minimum Does Not Guarantee Approval

One of the biggest misconceptions among first time buyers involves the mortgage credit score minimum.

Meeting a minimum score does not automatically result in mortgage approval.

Lenders also review:

Stable Income

Reliable income helps demonstrate repayment ability.

Employment History

Consistent employment often strengthens an application.

Debt Management

Reasonable debt obligations improve qualification potential.

Cash Reserves

Additional savings may strengthen overall financial stability.

Property Eligibility

The home itself must satisfy FHA property requirements.

A balanced financial profile generally creates stronger approval opportunities than relying on credit score alone.

Mortgage Credit Score Needed for Better Loan Terms

Another important consideration is the mortgage credit score needed to access favorable financing.

Generally speaking, stronger credit profiles may provide:

- Greater lender flexibility

- More financing options

- Improved interest rate opportunities

- Easier underwriting

- Better long term affordability

Improving credit before purchasing a home can often generate meaningful savings over the life of a mortgage.

Typical Credit Profile Comparison

Every lender evaluates borrowers individually.

Why FHA Loans Are Popular Among First Time Buyers

FHA financing continues to attract many Washington homebuyers because of its accessibility.

Benefits often include:

Flexible Qualification Standards

FHA programs frequently accommodate a wider range of borrowers.

Lower Down Payment Opportunities

Qualified buyers may benefit from lower upfront cash requirements.

Competitive Financing Options

Many first time buyers find FHA loans easier to qualify for than certain conventional programs.

Expanded Homeownership Access

Borrowers with limited credit history often find FHA financing more attainable.

These advantages continue making FHA loans one of the most widely used first time homebuyer programs.

How Lenders Evaluate Credit Beyond the Score

Your numerical score represents only part of your credit profile.

Underwriters also review:

Payment History

Consistent on time payments demonstrate financial responsibility.

Credit Utilization

Lower revolving balances generally strengthen credit profiles.

Length of Credit History

Longer credit histories provide additional performance data.

Recent Credit Activity

Multiple new accounts may receive additional review.

Outstanding Collections

Certain credit events may require explanation depending on lender requirements.

Key Takeaway

A mortgage approval decision considers your complete credit history, not simply the three digit credit score.

How First Time Buyers Can Improve Mortgage Readiness

Preparing several months before applying can improve qualification opportunities.

Make Payments on Time

Payment history remains one of the strongest contributors to credit health.

Reduce Credit Card Balances

Lower utilization may improve credit scores over time.

Avoid Opening New Credit Accounts

Limiting new debt before applying can strengthen applications.

Review Credit Reports

Correcting reporting errors may improve qualification potential.

Build Emergency Savings

Cash reserves often strengthen overall financial stability.

Pro Tip

If you plan to purchase a home within the next year, begin preparing your credit profile early. Small improvements made months before applying can produce meaningful financing benefits.

Common Credit Mistakes Before Applying for an FHA Loan

Many borrowers unintentionally weaken their mortgage applications.

Common mistakes include:

Missing Payments

Even one late payment can affect lender confidence.

Financing Large Purchases

New vehicle or furniture financing increases debt obligations.

Closing Older Credit Accounts

Older accounts often contribute positively to credit history.

Applying for Multiple Loans

Numerous credit inquiries within a short period may raise questions.

Ignoring Credit Report Errors

Reviewing reports early allows time for corrections before applying.

Why Credit Scores Matter More in Higher Cost Markets

Washington home prices often exceed national averages.

Larger mortgage amounts mean lenders carefully evaluate borrower qualifications.

Maintaining a strong credit profile may improve financing opportunities in competitive housing markets such as:

- Seattle

- Bellevue

- Redmond

- Tacoma

- Kirkland

- Spokane

Strong financial preparation becomes particularly valuable when purchasing higher priced homes.

FHA Loans Versus Conventional Credit Requirements

Many first time buyers compare FHA financing with conventional mortgages.

FHA Loans

Often appeal to borrowers seeking:

- Flexible qualification standards

- Lower down payment opportunities

- Expanded access to financing

Conventional Loans

May appeal to borrowers with:

- Strong credit profiles

- Larger down payments

- Higher household incomes

The best mortgage program depends on each borrower's complete financial picture rather than credit score alone.

Key Takeaway

FHA loans continue providing valuable financing opportunities for many Washington first time buyers who may not yet qualify for every conventional mortgage option.

Why I Think Too Many Buyers Focus Only on Their Credit Score

One of the first questions I hear from prospective homeowners is:

"What credit score do I need?"

While that is an important question, it is rarely the only one that matters.

Successful mortgage approval is built on a complete financial profile.

Income, employment, savings, debt management, and documentation all work together with your credit history.

I have seen borrowers with average credit receive mortgage approval because their overall financial picture was strong. I have also seen borrowers with higher credit scores experience challenges because of excessive debt or unstable income.

Instead of chasing a specific number, focus on building a healthy financial foundation. That approach often produces better mortgage outcomes and greater confidence throughout the home buying process.

— Max Nasab

Explore FHA Mortgage Options With PaloRate

PaloRate helps Washington first time buyers understand FHA loan requirements, evaluate mortgage options, and prepare for successful homeownership.

Whether you are just beginning your home search or preparing to apply for financing, understanding how lenders evaluate mortgage credit scores can help you move forward with greater confidence.

FAQ

What is a mortgage credit score?

A mortgage credit score is a lender reviewed credit profile used to evaluate a borrower's financial responsibility and mortgage qualification.

What FHA mortgage credit score is required?

The FHA establishes minimum eligibility standards, while individual lenders may apply additional qualification requirements based on the overall borrower profile.

Does meeting the mortgage credit score minimum guarantee approval?

No. Lenders also evaluate income, employment, debt, assets, and other financial factors.

What mortgage credit score is needed for better loan terms?

Stronger credit profiles generally provide greater financing flexibility and may improve borrowing opportunities.

Can first time buyers qualify for FHA loans with limited credit history?

Yes. FHA financing often provides opportunities for qualified first time buyers who have limited credit history or developing credit profiles.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

Take your first step towards your home loan journey

Get a quote

.svg)

.svg)

.svg)

.svg)

.svg)