.avif)

Mortgage News

VA IRRRL Rates in Washington: How Much Can You Save With a Streamline Refinance

For many homeowners, refinancing is about lowering monthly payments or reducing long term interest costs. For eligible veterans in Washington, the VA Interest Rate Reduction Refinance Loan, commonly known as IRRRL, offers one of the simplest ways to achieve this.

Understanding how VA IRRRL rates work and how much you can actually save is essential before moving forward.

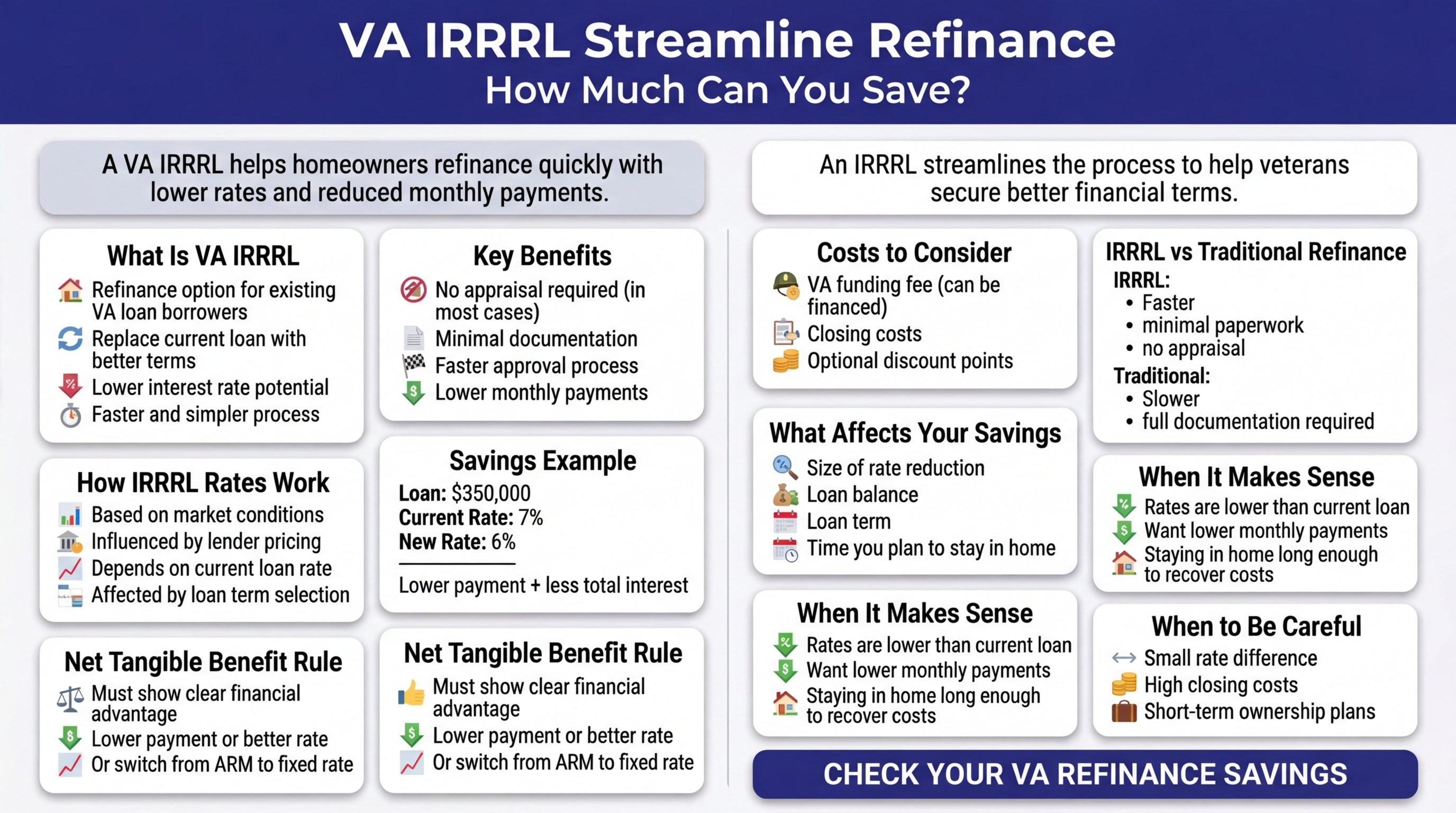

What Is a VA IRRRL

A VA IRRRL is a refinance option designed specifically for existing VA loan borrowers. It allows you to replace your current VA loan with a new one that typically has better terms.

Key benefits include:

- No appraisal required in most cases

- Minimal documentation

- Faster processing compared to standard refinance

- Ability to lower your interest rate

This is why it is often referred to as a streamline refinance.

How VA IRRRL Rates Work

Interest rates for IRRRL loans are usually lower than standard refinance options. However, rates still depend on several factors:

- Current market conditions

- Your existing loan rate

- Lender pricing

- Loan term selection

When researching va loan irrrl rates, it is important to compare multiple lenders because rate differences can impact your total savings.

Current Rate Trends in Washington

Washington borrowers are seeing:

- Moderate rate levels compared to previous years

- Fluctuations based on inflation and economic policies

- Differences between lenders depending on pricing models

Even a small reduction in your interest rate can lead to significant savings over time.

How Much Can You Save With an IRRRL

The savings depend on your current loan details and the new rate you qualify for.

Example Scenario

Even a 1 percent reduction in rate can lower monthly payments and reduce long term interest costs.

Key Requirement: Net Tangible Benefit

The VA requires that the refinance provides a clear financial advantage.

This is called a net tangible benefit, which usually means:

- Lower monthly payment

- Lower interest rate

- Switching from adjustable to fixed rate

Without this benefit, the loan may not be approved.

Costs Associated With IRRRL

Although the process is simplified, there are still some costs involved.

Funding Fee

Most borrowers must pay a small VA funding fee, which can be rolled into the loan.

Closing Costs

These may include lender fees and other standard charges.

Discount Points

Some borrowers choose to pay points to secure a lower interest rate.

IRRRL vs Traditional Refinance

The IRRRL process is designed to be more efficient and less burdensome.

Factors That Influence Your Savings

Rate Reduction

The bigger the difference between your current rate and new rate, the greater the savings.

Loan Term

Switching to a shorter term may increase monthly payments but reduce total interest.

Remaining Loan Balance

Higher balances typically result in larger savings from rate reductions.

Time in Home

Long term homeowners benefit more from refinancing savings.

When an IRRRL Makes Sense

A VA IRRRL may be a good option if:

- Current rates are lower than your existing rate

- You want to reduce monthly payments

- You plan to stay in your home long enough to recover closing costs

When to Be Careful

Refinancing may not be ideal if:

- The rate difference is very small

- Closing costs outweigh potential savings

- You plan to move soon

Careful evaluation is important before proceeding.

Tips to Maximize Savings

- Compare multiple lenders before choosing

- Consider rolling costs into the loan

- Evaluate long term savings, not just monthly payment

- Lock your rate at the right time

Frequently Asked Questions

1. What are VA IRRRL rates

They are interest rates offered for VA streamline refinance loans, typically lower than standard refinance rates.

2. Do I need an appraisal for IRRRL

In most cases, an appraisal is not required, making the process faster and easier.

3. Can I reduce my loan term with IRRRL

Yes, but you must still meet the net tangible benefit requirement.

4. How much can I save with an IRRRL

Savings depend on your current rate, new rate, and loan balance. Even small rate reductions can lead to significant savings over time.

5. Is the VA funding fee required

Yes, most borrowers must pay a funding fee, but it can often be included in the loan amount.

Final Thoughts

VA IRRRL loans provide a simple and effective way for Washington homeowners to reduce their mortgage costs. With lower rates, minimal documentation, and faster processing, this option can deliver meaningful savings when used correctly.

Understanding va loan irrrl rates, comparing lenders, and evaluating your long term plans will help you decide if a streamline refinance is the right move.

Get a free instant rate quote

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

Take your first step towards your home loan journey

Get a quote

.svg)

.svg)

.svg)

.svg)

.svg)